The day a teen gets a permit or license in Georgia usually feels the same in every family. The student is excited. The parent is proud, and a little nervous. Then the practical questions start coming fast. Whose car will they drive? How much practice do they need? What insurance do we need before they head out on their own?

That last question trips up a lot of people because insurance language can sound more complicated than it really is. But the liability insurance basics are simpler than they look once you connect them to real driving. If a new driver makes a mistake and hurts someone or damages someone else's property, liability insurance is the part of the policy that helps pay for the damage the driver caused.

For Georgia families, that matters for two reasons. First, driving legally means having the right coverage in place. Second, learning to drive well can affect how manageable insurance feels over time. Good habits behind the wheel don't just make the road safer. They can also help families make better insurance choices.

You Have the Keys Now What About Insurance

A lot of teens think getting a license is the finish line. It's really the start of a new responsibility.

You've studied signs, practiced turns, worked on parking, and learned how to handle traffic. Then the license comes, and suddenly the bigger world opens up. School, work, practice, errands, visiting friends. Freedom gets very real, very fast.

For parents, the same moment can feel different. You're proud, but you're also thinking about risk. A teen driver doesn't need to be reckless to have a problem. A missed stop sign, a rushed left turn, or a bump in a crowded parking lot can create real bills and real stress.

That's why insurance belongs in the same conversation as safe driving practice. It isn't just paperwork. It's part of being ready for the road.

Why this feels confusing

Most families don't struggle because insurance is impossible to understand. They struggle because the words sound abstract. Terms like liability, coverage limits, claim, and premium don't feel connected to everyday driving until you put them into a simple example.

Say a teen backs out too quickly and hits another car. Nobody plans for that. But once it happens, money becomes part of the situation right away. Who pays for the repair? What if someone is injured? What if the other driver says their neck hurts later and files a claim?

Those are liability insurance questions.

Practical rule: If your driving causes harm to someone else, liability insurance is the part of your policy built to respond.

Parents also often want to know whether adding a teen driver will raise the family's cost. That concern is common, and it helps to start with a clear overview like this guide on whether having your teen on your insurance can raise your rates.

Insurance may not feel as exciting as getting the keys, but it's part of true independence. A driver isn't fully prepared just because they can move a car safely. They also need the financial protection that goes with driving on public roads.

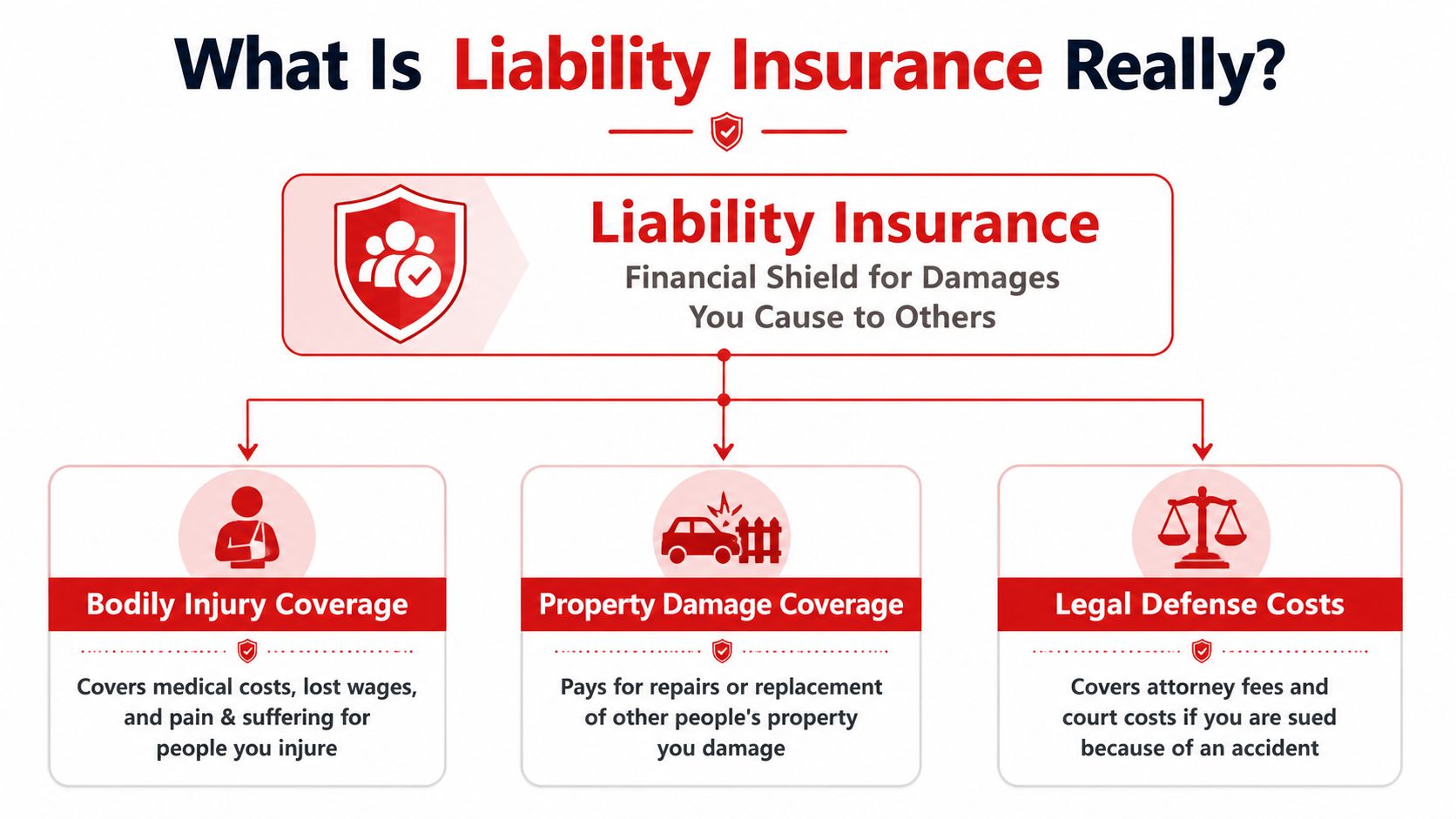

What Is Liability Insurance Really

Liability insurance is financial protection for damage you cause to other people. That's the cleanest way to think about it.

If you're at fault in a crash, liability insurance generally helps with the other person's losses. It is not mainly there to fix your own car or pay your own injuries. It's there because driving carries responsibility. When your mistake harms someone else, the policy can step in.

The two parts most families need to know

The simplest breakdown is this:

- Bodily injury liability pays toward injuries suffered by another person after an at-fault accident.

- Property damage liability pays toward damage you cause to someone else's car or other property.

Think of liability insurance like a financial shield you carry while driving. You hope you never need it. But if you make a mistake, it can protect your family from having to pay the full amount directly out of pocket.

A basic example helps. If a teen rear-ends another driver at a red light, the other driver may need medical care and their car may need repairs. Bodily injury liability connects to the injury side. Property damage liability connects to the repair side.

When coverage applies

Coverage doesn't apply to every bad thing that happens in every situation. The Insurance Information Institute explains that coverage applies when the damage or injury is caused by an “occurrence”, meaning an accident, happens within the “coverage territory”, and occurs during the “policy period” when the insurance is active, which helps explain why liability coverage is meant for unexpected accidents rather than intentional acts in this overview of liability insurance terms.

That's a useful filter for teen drivers and parents. Insurance is built for accidents. It is not a free pass for intentional damage or reckless choices made on purpose.

Liability insurance follows the idea of responsibility, not convenience. If the policy is active and the event fits the covered kind of accident, the policy may respond.

One detail many beginners miss

A lot of starter explanations focus only on crashes and repair bills. That leaves out a real part of general liability coverage in other settings. Some policies can also involve personal and advertising injury, such as libel, slander, false arrest, and copyright infringement in advertising. One verified summary notes that 28% of general liability claims involve non-physical injuries like advertising injury or personal harm in this discussion of general liability lessons. That comes up more often in business coverage than personal auto, but it's a helpful reminder that “liability” isn't always limited to dents and doctor bills.

If you want a broader, plain-English explanation of how this works outside auto policies too, this article on liability insurance for your business gives a useful comparison point.

For a driving-specific breakdown that keeps the focus on families and new drivers, this car insurance guide for Georgia drivers can help connect the terms to actual auto coverage decisions.

Georgia's Minimum Insurance Requirements

Georgia drivers need liability coverage to drive legally. Families often hear the shorthand first, then wonder what the numbers mean in real life.

The common shorthand is 25/50/25. That's the state minimum auto liability requirement often discussed for Georgia drivers. It refers to bodily injury coverage per person, bodily injury coverage per accident, and property damage coverage per accident.

What the minimum numbers mean

Here's the simple version.

| Coverage Type | Minimum Limit |

|---|---|

| Bodily Injury Liability per person | $25,000 |

| Bodily Injury Liability per accident | $50,000 |

| Property Damage Liability per accident | $25,000 |

Those numbers matter because they set the legal floor, not necessarily the safest financial choice for every family.

If one person is injured, the per-person bodily injury limit applies. If multiple people are injured in the same accident, the per-accident bodily injury cap matters. Property damage is separate and applies to what you damage, such as another vehicle, a fence, or other property.

Why minimum doesn't always mean enough

Many new drivers often get confused. They assume “legal minimum” means “good protection.” It doesn't always.

A moderate accident can involve more than one vehicle, more than one injured person, or significant property damage. Once the policy limit is exhausted, the remaining costs may not disappear. They can become the driver's responsibility.

Important takeaway: State minimum coverage gets you to the legal starting line. It may not be enough to protect your savings, income, or household finances after a serious wreck.

A parent can think of it this way. Minimum limits are like bringing the smallest umbrella because the forecast says “chance of rain.” It may satisfy the basic requirement, but it won't feel like enough when the storm gets stronger.

How to use the minimum wisely

The best approach is to treat Georgia's minimum as a reference point, then ask practical questions:

- How much would another car cost to repair or replace? Many vehicles on the road today can create property damage bills that rise quickly.

- Could more than one person be hurt? Even a single mistake at an intersection can affect multiple people.

- What could our family realistically pay if insurance ran out? That answer helps frame whether higher limits make sense.

This isn't about fear. It's about honesty. New drivers are still building judgment. Parents are balancing safety and budget. Knowing the minimum helps, but understanding its limits helps more.

Understanding Coverage Limits and Premiums

Insurance prices can feel random when you first look at them. They aren't random. They reflect how much protection you buy and how much risk the insurer believes it's taking on.

Two terms matter right away: coverage limits and premiums. The limit is the amount the policy may pay up to for a covered loss. The premium is what you pay for the policy.

What a limit really does

A policy doesn't promise to pay forever. It promises to pay up to listed amounts.

One verified industry explanation notes that insurance policies have a per occurrence limit, meaning the maximum paid for one accident, and sometimes an aggregate limit, meaning the total maximum paid during a policy term. It also notes that for auto insurance, understanding your per-occurrence limit is especially important because it's the most you're covered for in a single incident, as explained in this guide to liability insurance requirements.

That's a key part of liability insurance basics. If a crash creates losses above your policy limit, the extra amount doesn't automatically become the insurer's problem.

Why one family pays more than another

Insurers price policies based on risk. A new teen driver usually looks different to an insurer than an experienced adult with a long clean driving history. The company is estimating how likely a claim may be and how expensive it could become.

Common factors often include:

- Driving experience because newer drivers have less time on the road

- Vehicle type because some cars cost more to repair or replace

- Where and how the car is driven because daily use patterns matter

- Chosen limits because more protection usually costs more

Not every factor is under your control, but some are. That's good news for families who want to make insurance more manageable over time.

Higher limits and higher premiums

In general, higher protection means a higher premium. That part makes sense. If the insurer may have to pay more after a serious loss, it usually charges more for that promise.

But the smart question isn't “How do we buy the absolute cheapest policy?” The smart question is “How much protection do we need, and what can we do to look like a safer risk?”

That shift matters. Families who understand insurance as something they can influence tend to make better choices than families who see it only as a fixed bill they're stuck with.

A premium is not just a price tag. It's also a reflection of how prepared, trained, and risky the driver appears on paper.

If you're helping a teen compare options, ask for the quote details in writing and review the limits line by line. Don't focus only on the monthly payment. The monthly payment matters, but the coverage behind it matters more.

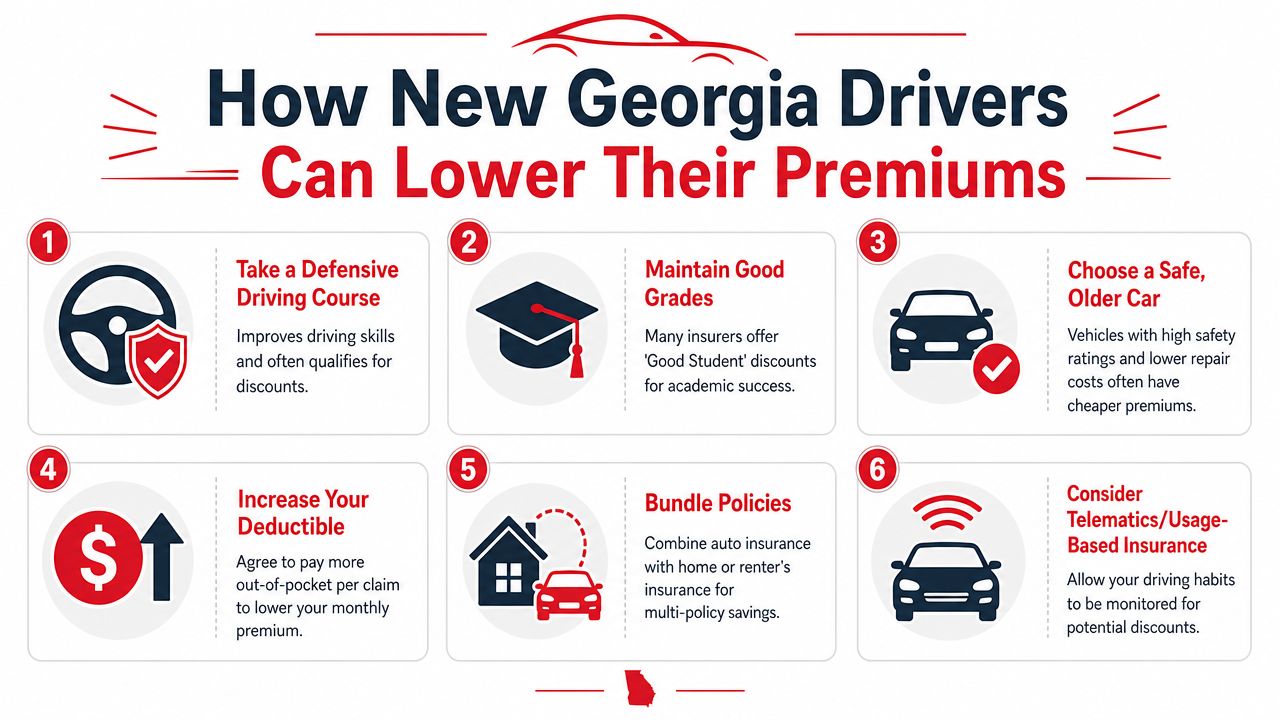

How New Georgia Drivers Can Lower Their Premiums

The most practical way to lower insurance pressure is to lower risk. That starts long before a claim. It starts with training, judgment, and daily driving habits.

Families often look first for discounts, and that's reasonable. But the bigger long-term win is building a driver who makes fewer mistakes, handles pressure better, and approaches the road with discipline.

Start with driver education

Georgia families should know one requirement clearly. Under Joshua's Law, 16- and 17-year-olds must complete a DDS-approved 30-hour Driver's Education course before applying for a Class D license, as outlined in this explanation of Joshua's Law in Georgia.

That classroom requirement matters on its own because it's part of the licensing path. It can also matter financially because many insurers reward completed driver education.

For busy families, online learning can make that requirement easier to fit into a real schedule. A flexible online course can help a student complete the classroom portion while still keeping up with school, sports, and family obligations.

Build skill where it counts most

Classroom learning is valuable, but on-road training is where many teens become calmer and more consistent. That's where they practice lane control, intersections, turns, parking, mirror use, speed management, and decision-making under pressure.

A few areas make a big difference for new drivers:

- Parking lot control: Low-speed mistakes can still produce expensive property damage claims.

- Intersections: Many early driving errors happen when drivers rush judgments.

- Lane changes and merging: Confidence helps, but proper timing and scanning matter more.

- Road test preparation: A student who's prepared for the test is often better prepared for real solo driving too.

Here's a quick visual summary families may find useful before comparing options:

Other practical ways families save

Not every cost-saving step comes from the classroom, but education helps families make smarter choices in all of them.

- Good student discounts: Some insurers reward strong academic performance.

- Vehicle choice: A modest, safety-focused vehicle is often easier to insure than a car that's expensive to repair.

- Policy bundling: Parents sometimes lower overall household cost by combining policies.

- Driving monitoring programs: Some insurers offer savings when families opt into programs that track driving behavior.

If you want an outside example of the kinds of steps people take to compare options and reduce costs, this article about saving on car insurance in WA is a useful cross-check, even though Georgia rules and quotes will differ.

For Georgia-specific ideas, this guide on how to lower car insurance premiums is directly relevant to new drivers and their parents.

Make training affordable enough to finish

Families sometimes delay lessons because they're focused on the cost right now, even though stronger training can support safer driving afterward. If budget is the obstacle, look into the Georgia Driver's Education Scholarship Grant Program and ask whether you qualify. Programs like that can make it easier to complete the education and driving lessons a new driver needs.

The main point is simple. If you want a lower premium over time, become the kind of driver insurers worry less about. That starts with proper education, consistent practice, and enough real instruction behind the wheel that the student isn't guessing once they're alone.

Navigating the Claims Process After an Accident

Even careful drivers can end up in a crash. When that happens, panic makes people do the wrong things. A simple routine helps.

The first priority is safety. Check yourself, check passengers, and check the other people involved. If vehicles can be moved safely and local conditions allow it, get out of the flow of traffic.

What to do at the scene

Use a basic checklist:

- Check for injuries first. If anyone may be hurt, call 911.

- Move to safety if possible. Don't create a second accident by staying in a dangerous spot.

- Exchange information. Get names, contact details, driver's license details, vehicle information, and insurance information.

- Take photos. Capture damage, license plates, the roadway, traffic signs, and the overall scene.

- Notify police when needed. If there are injuries, serious damage, or any uncertainty, involving law enforcement helps create a record.

What not to say

A lot of teens are raised to be polite, so their first instinct is to apologize. That instinct is understandable, but it can create problems.

Don't argue. Don't guess. Don't say “It was all my fault” at the scene. Give factual information and let the insurers and investigators sort out responsibility.

After a crash, trade facts, not conclusions.

Starting the insurance claim

Once everyone is safe and the immediate scene is handled, contact your insurance company as soon as you can. Be ready to provide the date, time, location, photos, the other driver's details, and any police report information.

Your insurer may ask follow-up questions, request documents, or explain what happens next. Cooperate fully and keep your records organized. Save screenshots, claim numbers, names of representatives, and copies of any messages or forms.

One more practical tip for parents. If a teen is involved in a crash, stay calm when you speak with them. A shaken driver may forget details or make confused statements if they feel they're about to get in trouble. The goal in that moment is safety, accurate information, and a clean next step.

Your Next Steps to Become a Safe and Insured Driver

Liability insurance basics come down to one idea. Driving doesn't just create freedom. It creates responsibility.

A policy helps protect other people if you cause harm, and it helps protect your family from the financial shock that can follow an accident. But the strongest insurance strategy doesn't start with shopping for the cheapest quote. It starts with becoming a safer, better-prepared driver.

For Georgia teens and parents, that means turning knowledge into action:

- Complete Joshua's Law training so the licensing process starts on solid ground.

- Invest in real driving lessons and lesson packages so the student gains skill, not just seat time.

- Prepare carefully for the road test so the new driver enters solo driving with better habits and more confidence.

A driver who learns well, practices seriously, and respects the road is usually in a better position both legally and financially.

If you're ready to move from reading about insurance to building real driving confidence, A-1 Driving School offers Georgia teen and adult driver's education, DDS-approved Joshua's Law courses, online course options, driving lessons, driving lesson packages, road test support, and information about the Georgia Driver's Education Scholarship Grant Program. For families who want one clear path from classroom learning to behind-the-wheel practice to road testing, it's a practical place to start.