Your renewal notice shows up, and the premium is higher again. For a lot of Georgia drivers, that feels random. It isn't.

Insurance companies price risk. Some parts of that price are hard to control in the short term, but many aren't. You can lower the bill by adjusting the policy you already have, shopping the market carefully, and building the kind of driving record and skill profile insurers want to see.

The mistake I see most often is treating insurance like a fixed monthly expense, the same way you'd treat a utility bill. It's not. It's a moving number tied to your car, your mileage, your coverage choices, and how confidently an insurer thinks you'll avoid claims.

For teen drivers and families in Georgia, there's another piece people overlook. Driver education and professional lessons don't just help someone pass a test. They help produce fewer bad habits, cleaner records, and better decisions behind the wheel. That matters when you're trying to figure out how to lower car insurance premiums for the long run.

Why Your Car Insurance Bill Is So High and What You Can Do

High premiums usually come from a mix of exposure and policy design. If you drive a lot, carry low deductibles, insure a newer vehicle with full physical damage coverage, or have a newer driver on the policy, the price climbs. In Georgia, that can hit families especially hard when a teen is preparing to get licensed or has just started driving independently.

The good news is that a premium isn't a punishment carved in stone. It's a quote based on inputs. Change the inputs, and you often change the price.

Three levers you can actually control

I'd break the problem into three parts:

Policy changes you can make now

Deductibles, coverage on older cars, payment setup, and bundled policies all affect what you pay.Shopping with precision

If you compare sloppy quotes, you get sloppy answers. If you compare the same policy across carriers, you can spot real savings.Skill and record over time

This is the long game. Better training usually leads to better driving decisions, which can help drivers stay claim-free and violation-free.

Practical rule: If you don't know exactly what coverages you're paying for, you're not ready to judge whether your premium is too high.

Some drivers also start from a tougher position because of past violations, limited driving history, or a nonstandard policy. If that's your situation, A-1's guide on insurance options for high-risk drivers in Georgia can help you understand what insurers tend to look at and where you still have room to improve.

What usually works and what usually doesn't

Here's the short version.

| Approach | Usually worth doing | Main trade-off |

|---|---|---|

| Comparing quotes | Yes | Takes time and paperwork |

| Raising deductible | Often | Higher out-of-pocket cost after a claim |

| Bundling policies | Often | One insurer may not be cheapest for every line |

| Dropping coverage on an older car | Sometimes | You absorb damage to your own vehicle |

| Professional driver training | Strong long-term move | Requires time and upfront cost |

| Chasing tiny add-ons only | Usually not enough | Savings may be too small by themselves |

A lot of people look for one trick. There usually isn't one. The lower premium comes from stacking smart decisions.

Start Saving Now With These Policy Adjustments

A Georgia driver gets the renewal notice, sees the premium jump, and assumes the only fix is shopping for another company. Sometimes you can cut the bill faster by tightening the policy you already have first.

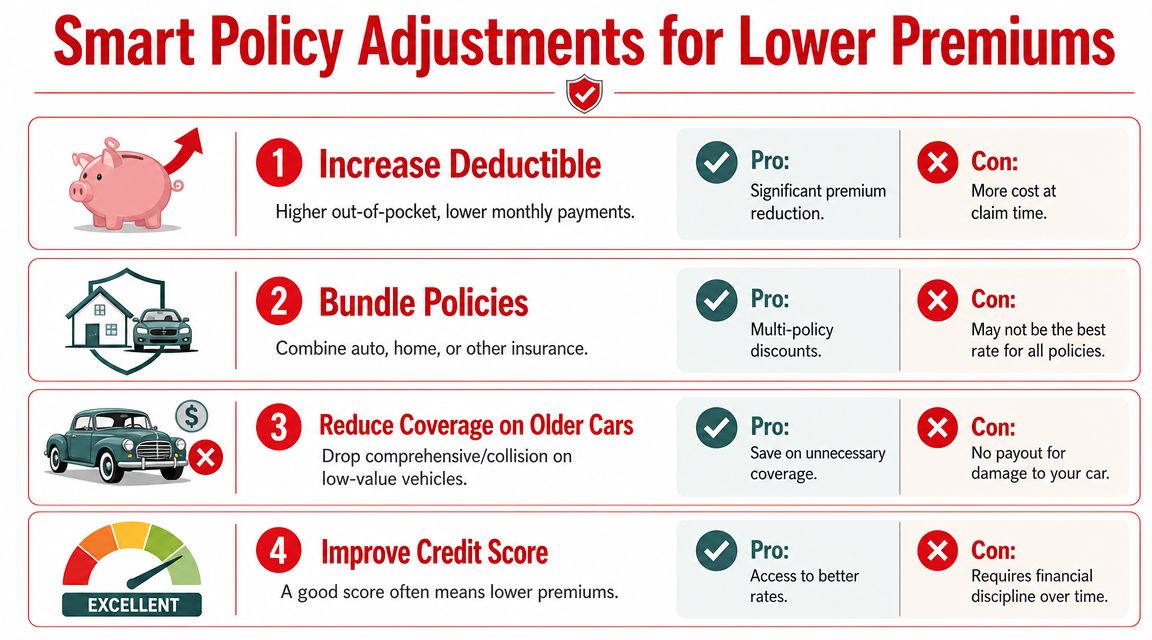

Raise your deductible only if you can pay it tomorrow

Higher deductibles usually bring the premium down because the insurer pays less on smaller claims. Consumer Reports found that increasing a deductible from $500 to $1,000 can produce meaningful savings in some cases, which is why it remains one of the standard recommendations in its reporting on how to lower car insurance rates.

The trade-off is simple. If you back into a pole next week, can you cover that higher amount without putting the repair on a credit card?

From an instructor's point of view, this works best for drivers who have built better habits and are less likely to file small collision claims. If you are still rebuilding after tickets, crashes, or a shaky first year of driving, a higher deductible can save money on paper while making a real-world claim much harder to absorb.

Review physical damage coverage on older cars

Collision and other perils coverage make more sense on a newer vehicle with real replacement value. On an older car, the math can turn against you fast.

The National Association of Insurance Commissioners advises drivers to compare the cost of those coverages against what the car is worth in its consumer guide to auto insurance basics and coverage decisions. If the annual premium for covering damage to your own car is getting too close to the vehicle's value, keeping full coverage may stop being practical.

That does not mean every older car should lose coverage. A dependable paid-off car still has value if you cannot replace it easily. The right question is whether you could handle the loss yourself.

Bundle carefully and check the fees

Bundling auto with renters or home insurance can reduce the total bill. So can changing how you pay. Progressive notes that policyholders may save through multi-policy discounts and by choosing payment setups that reduce extra charges in its overview of car insurance discounts and savings options.

Check three things before you accept the offer:

- The total household cost, not just the auto premium

- Installment or billing fees, especially if you pay monthly

- Coverage changes that make one quote look cheaper than it really is

If you want a second reference point before you call your insurer, A-1 has a practical guide with car insurance tips for Georgia drivers.

Give special attention to discounts tied to driver behavior

Policy adjustments help right away, but the strongest savings usually show up when the insurer sees a lower-risk driver on the page. That is where Georgia drivers miss the bigger opportunity.

Many carriers reward a clean record, defensive driving, or other approved driver education steps. The Georgia Office of Commissioner of Insurance and Safety Fire encourages drivers to ask insurers directly about available discounts and rating factors in its consumer information on auto insurance in Georgia. In practice, that means a driver who improves skill, avoids violations, and stays claim-free often has more room to save over time than a driver who only tweaks deductibles.

That is also why I tell students to treat policy changes as the short play and training as the long play. A lower premium built on better driving decisions tends to last longer than a discount built on one billing change.

If you want to compare offers after you clean up the policy details, use the same coverage settings each time and compare Georgia car insurance rates with the numbers lined up evenly.

How to Shop for Car Insurance in Georgia

A Georgia driver gets two quotes that look far apart, then finds out the cheaper one raised the deductible, dropped roadside coverage, and rated the car for pleasure use instead of a daily commute. I see this kind of mismatch all the time. If you want a real price comparison, every quote has to be built on the same facts.

Start with your current declarations page and use it as the template. That single document keeps the shopping process honest because it shows the limits, deductibles, listed drivers, and optional coverages you already carry. The Insurance Information Institute advises drivers to get at least three quotes, and the National Association of Insurance Commissioners explains in its consumer guide on shopping for auto insurance that price comparisons only mean something when the coverage is matched closely.

Bring these details with you before you request quotes:

- Your declarations page from the current policy

- Vehicle information for each car

- Driver information for every household driver who needs to be listed

- Current coverage selections, including deductibles and add-ons

- Estimated annual mileage and primary vehicle use

That last item matters more than drivers expect. A car used for commuting is rated differently from one used mostly for errands or school. If the usage is wrong, the quote may look good now and change later.

Make it an apples-to-apples comparison

Keep every quote on the same settings. Match bodily injury limits, property damage limits, uninsured motorist choices, collision and non-collision deductibles, rental reimbursement, and every rated driver.

| Item to match | Why it matters |

|---|---|

| Liability limits | Lower limits reduce the premium but also reduce protection |

| Collision and comprehensive deductibles | Higher deductibles can make one quote look cheaper on paper |

| Included drivers | Omitting a household driver can distort the real cost |

| Vehicle use | Commute, school, and pleasure use are priced differently |

| Annual mileage | Some insurers rate lower-mileage drivers more favorably |

Cheap and equivalent are not the same thing.

Ask questions that expose the real price

A useful call with an agent should sound more like an audit than a casual quote request. Ask what discounts are already applied, whether installment fees are added for monthly billing, whether a low-mileage option is available, and how a telematics program affects both price and privacy. Consumer Reports notes in its reporting on how comparison shopping lowers car insurance rates that insurers often price the same driver very differently, which is exactly why the details have to stay fixed from quote to quote.

I also tell Georgia families to ask one question many people skip: “How will this company treat a newly trained or newly improved driver over time?” The lowest quote today is not always the best value next renewal. A company that responds well to a clean record, completed driver education, and fewer violations can save you more over the next few years than a carrier that starts low and climbs fast.

If you want a practical checklist before making calls, A-1 has a Georgia car insurance guide for drivers and families that lays out what to review on a policy before you compare offers. You can also compare Georgia car insurance rates to get a market snapshot before you start lining quotes up side by side.

The cheapest quote only helps if it covers the same risk.

Invest in Your Skills The Ultimate Georgia Insurance Discount

The biggest mistake families make with a new driver is focusing only on the policy. The policy matters, but the driver matters more.

A lower premium over time usually follows a lower-risk profile. That starts with training. Not rushed practice in a parking lot. Not guessing your way through lane changes, merges, and scanning habits. Actual instruction.

Why training changes the insurance conversation

Insurers reward signs that a driver is less likely to create a claim. Some discounts are immediate and policy-based. Others show up indirectly because the driver avoids tickets, avoids crashes, and builds a cleaner record.

That's why I put driver education and professional lessons above most one-time insurance hacks for teen families. A higher deductible can reduce your premium this month. Better driving habits can affect what you pay for years.

The strongest version of this in Georgia is structured training tied to the licensing path. For teens, that often means a Joshua's Law-compliant course, behind-the-wheel instruction, and continued practice that builds real road skill instead of test-only skill.

Where Georgia families often save the most frustration

Parents usually want two things at once. They want a teen licensed, and they want to avoid expensive mistakes right after licensing.

Professional instruction helps with the common weak points:

- Observation habits at intersections and during lane changes

- Speed control in traffic flow instead of overreacting

- Parking and backing without panic

- Road test readiness so the first months of driving aren't built on shaky basics

A teen who learns clean habits early is more likely to avoid the kind of errors that lead to citations and claims. That's the part many families miss when they ask only about discounts.

Here's a short video that walks through part of that path:

What to look for in a Georgia training path

If you're choosing training with insurance savings in mind, think in layers:

A recognized driver education course

This is the foundation for many teen drivers.Behind-the-wheel lessons

Classroom knowledge doesn't fix steering control, timing, or mirror use.Road test preparation and testing support

A driver who barely passes often still needs work. A driver who is properly prepared starts stronger.Flexible online options

Scheduling matters. Families are more likely to complete training when the format works.

Georgia families should also look into the Georgia Driver's Education Scholarship Grant Program if cost is part of the hesitation. That can make formal training more accessible, which matters because delaying instruction often leads families to rely on pieced-together practice that leaves gaps.

One practical option is A-1 Driving School, which offers Georgia driver's education, Joshua's Law courses, online class options, road test support, and driving lesson packages. For families trying to connect licensing, instruction, and long-term insurance savings, that kind of full path is usually more useful than treating each step separately.

Better driving skill won't guarantee a specific premium. It does put you in a stronger position to earn lower rates over time by avoiding the mistakes that push premiums up.

Lessons matter even for adults

This isn't just a teen issue.

Adult drivers who are new to Georgia roads, returning to driving after years away, or trying to correct bad habits can also benefit from formal lessons. In practice, adults often improve fastest when an instructor targets a narrow set of issues such as left turns in traffic, highway merging, gap judgment, or parallel parking.

That's not glamorous. It is effective. And effective is what lowers long-term risk.

Claim Every Georgia Car Insurance Discount You Qualify For

A lot of Georgia drivers do the hard parts right, then miss easy savings because the insurer is working from old information. I see this often with families adding a teen driver, adults who now drive fewer miles, and policyholders who finished a qualifying course but never sent in proof.

Discounts worth checking line by line

Call your insurer and ask for a discount review, not just a price check. Those are different conversations. A price check usually gives you the same policy with the same assumptions. A discount review forces the carrier to confirm what is and is not on file.

Start with discounts you can document:

- Good student discount if your student meets the grade requirement

- Low mileage discount if your annual driving has dropped

- Good driver or accident-free discount if your record supports it

- Multi-policy discount if you carry renters or homeowners coverage with the same insurer

- Vehicle feature discounts for safety or anti-theft equipment

- Course completion discount if your insurer gives credit for approved driver training

Ask what proof they need and when it takes effect. If a teen completed formal instruction in Georgia, or an adult finished a defensive driving course, send the certificate instead of assuming the system caught up on its own.

Check the car, not just the policyholder

Vehicle details can change the rating more than drivers expect. Factory safety features, anti-theft devices, and garage parking may all be worth confirming. If you changed cars recently or added theft deterrents, make sure the declarations page reflects that.

If you want a broader look at theft prevention options, this guide can help you compare car security systems.

Driver training deserves special attention

This is the discount area Georgia families overlook most.

Insurers do not all treat training the same way. Some give a direct discount for an approved course. Some price it indirectly by looking more favorably at the driver profile. Either way, professional instruction is one of the few savings steps that can help now and also reduce the mistakes that make premiums climb later.

For teen drivers, that matters a lot. For adults, it still matters. A short refresher course can correct habits that lead to claims, citations, or nervous driving decisions in traffic.

The Georgia Office of Commissioner of Insurance and Safety Fire encourages drivers to ask carriers about available discounts, including those tied to driver education and vehicle safety features, before renewing or changing a policy.

Focus on the discounts you can prove

I usually tell drivers to sort discounts into two groups:

| Discount type | What to do |

|---|---|

| Easy-to-document discounts | Verify each one is listed and submit proof if needed |

| Risk-based savings tied to training and vehicle details | Ask how the insurer evaluates them and update the file |

Small discounts help. The drivers who save more over time are usually the ones who combine careful policy review with better driving habits and formal instruction. In Georgia, that second part often gives you the stronger long-term payoff.

Your Action Plan for Lower Car Insurance Premiums

A Georgia driver can spend years overpaying by treating insurance like a bill that only goes up. It does not work that way. Premiums change when you adjust coverage, update your mileage, improve your driving record, and show insurers that the driver behind the wheel is less likely to file a claim.

Start with the steps that change price fastest, then work on the ones that lower risk over time.

This week

Pull up your declarations page and read it line by line. Confirm your deductibles, check whether each coverage still fits the car you drive, and flag any older vehicle carrying protection that no longer makes financial sense.

Then update the facts insurers use to price you. Fewer commute days, lower annual mileage, a completed driver education course, or a teen who has finished professional lessons can all change the quote you deserve.

Write down your questions before you call. Drivers save more when they ask specific questions than when they ask for “a better rate.”

This month

Get at least three quotes with the same coverage limits and deductibles. If the coverage changes from quote to quote, the comparison is useless.

Ask each insurer to review every discount, payment option, mileage program, and telematics option that fits your household. In Georgia, this is also the right time to ask how the company treats formal driver training. Some carriers apply a direct discount. Others price a trained driver more favorably even when they do not label it as a separate savings line.

If you want another consumer checklist for ways to reduce insurance premiums, compare it against your policy before you make changes.

The biggest long-term savings usually come from combining smart policy changes with better driving habits and documented training.

Over the next few months

For many Georgia families, the handling of teen driver training either saves money for years or locks in higher costs. If you have a teen driver, build the training plan early, before the license test is close and everyone is rushing. Structured practice, professional lessons, and solid road test preparation usually lead to fewer mistakes, fewer tickets, and a cleaner insurance record.

Adult drivers have opportunities here too.

A refresher lesson can fix the habits that lead to expensive claims, especially lane changes, following distance, backing, and left turns in heavy traffic. From an instructor's point of view, those are the mistakes that often look small until they show up on an insurance renewal.

The short version is simple. Review the policy. Shop the rate carefully. Invest in driving skills, because in Georgia that is one of the few steps that can help both now and later.

If you want help building that safer-driver profile, A-1 Driving School offers Georgia driver's education, Joshua's Law courses, online options, road test services, and driving lesson packages that help teens and adults build the road skills insurers want to see.